Fillable North Carolina 91C Template

Fillable North Carolina 91C Template

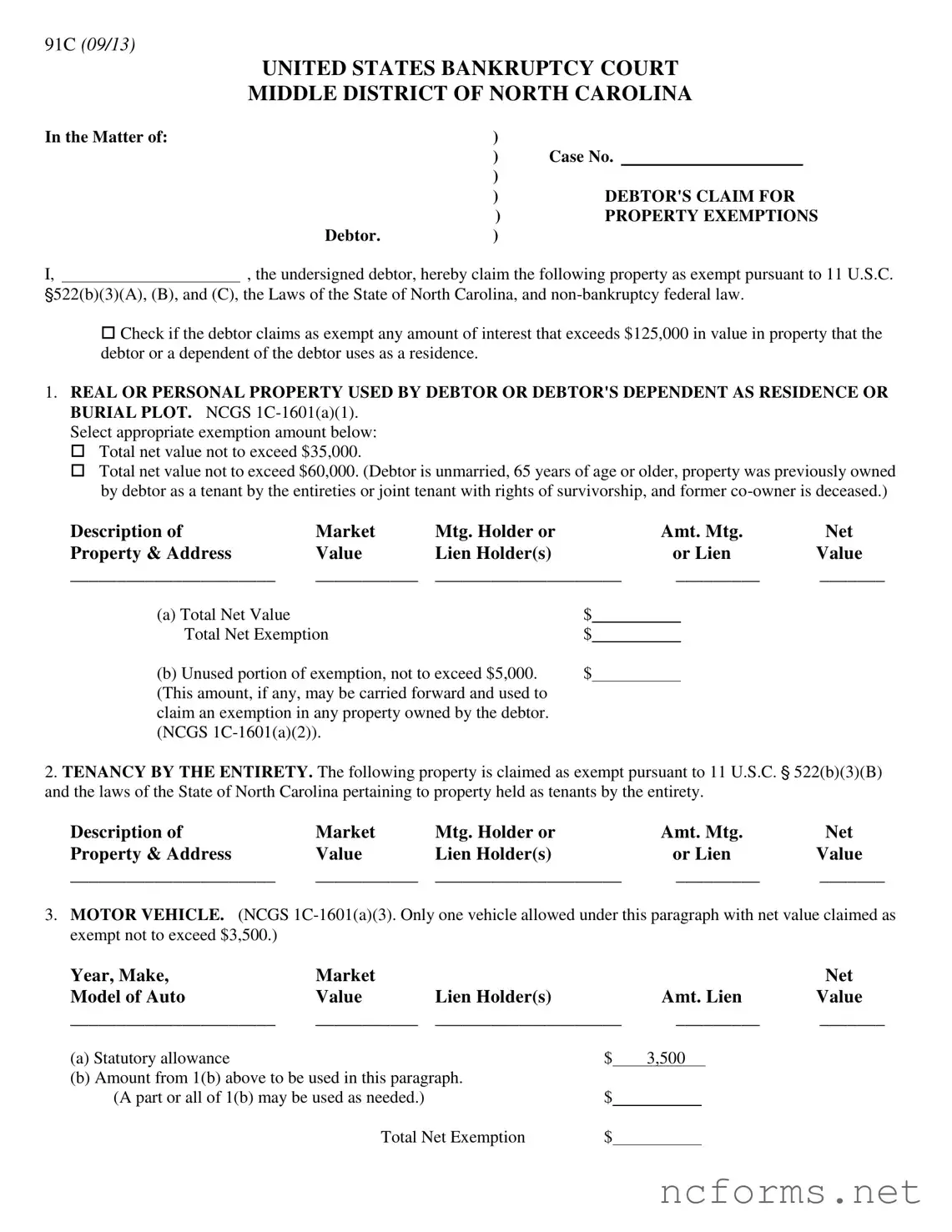

The North Carolina 91C form plays a pivotal role in the bankruptcy process, providing those facing financial distress with a tool to protect essential assets from creditor claims. This document, specific to the United States Bankruptcy Court for the Middle District of North Carolina, allows debtors to list and claim exemptions under both state and federal laws. These exemptions are critical for debtors seeking relief through bankruptcy, as they determine what property they can retain for a fresh start. The form encompasses a broad range of property types, from the debtor's residence or burial plot, vehicles, tools of trade, household goods, personal effects, to various types of compensation and retirement plans. Specifically, it details exemptions for real or personal property used as a residence, vehicles with a capped exemption value, essential tools for one's trade or profession, and personal property used for household needs, each with specified limits. Additionally, it addresses more nuanced categories like life insurance, professionally prescribed health aids, compensation for personal injuries, retirement and college savings plans, benefits from retirement plans of other states, support payments, and even certain benefits under non-bankruptcy federal law. This utilization of the 91C form underlines the tailored approach of bankruptcy laws to provide necessary protection to debtors, ensuring they do not emerge from the process entirely destitute, but instead have the means to rebuild their financial lives.

91C (09/13)

UNITED STATES BANKRUPTCY COURT

MIDDLE DISTRICT OF NORTH CAROLINA

In the Matter of: |

|

) |

|

|

|

|

|

|

|

) |

Case No. |

||

|

|

|

) |

|

|

|

|

|

|

) |

DEBTOR'S CLAIM FOR |

||

|

|

|

) |

PROPERTY EXEMPTIONS |

||

|

|

Debtor. |

) |

|

|

|

I, |

|

, the undersigned debtor, hereby claim the following property as exempt pursuant to 11 U.S.C. |

||||

'522(b)(3)(A), (B), and (C), the Laws of the State of North Carolina, and

Check if the debtor claims as exempt any amount of interest that exceeds $125,000 in value in property that the debtor or a dependent of the debtor uses as a residence.

1.REAL OR PERSONAL PROPERTY USED BY DEBTOR OR DEBTOR'S DEPENDENT AS RESIDENCE OR BURIAL PLOT. NCGS

Select appropriate exemption amount below:

Total net value not to exceed $35,000.

Total net value not to exceed $60,000. (Debtor is unmarried, 65 years of age or older, property was previously owned by debtor as a tenant by the entireties or joint tenant with rights of survivorship, and former

Description of |

Market |

Mtg. Holder or |

Amt. Mtg. |

Net |

Property & Address |

Value |

Lien Holder(s) |

or Lien |

Value |

______________________ |

___________ |

____________________ |

_________ |

_______ |

(a) Total Net Value |

$ |

|

|

Total Net Exemption |

$ |

|

|

(b) Unused portion of exemption, not to exceed $5,000. |

$ |

|

|

(This amount, if any, may be carried forward and used to |

|

|

|

claim an exemption in any property owned by the debtor. |

|

|

|

(NCGS |

|

|

|

2.TENANCY BY THE ENTIRETY. The following property is claimed as exempt pursuant to 11 U.S.C. ' 522(b)(3)(B) and the laws of the State of North Carolina pertaining to property held as tenants by the entirety.

Description of |

Market |

Mtg. Holder or |

Amt. Mtg. |

Net |

Property & Address |

Value |

Lien Holder(s) |

or Lien |

Value |

______________________ |

___________ |

____________________ |

_________ |

_______ |

3.MOTOR VEHICLE. (NCGS

Year, Make, |

Market |

|

|

|

|

|

|

Net |

Model of Auto |

Value |

Lien Holder(s) |

|

|

Amt. Lien |

Value |

||

______________________ |

___________ |

____________________ |

_________ |

_______ |

||||

(a) Statutory allowance |

|

|

$ |

|

3,500 |

|

|

|

(b) Amount from 1(b) above to be used in this paragraph. |

|

|

|

|

|

|

||

(A part or all of 1(b) may be used as needed.) |

|

$ |

|

|

|

|

|

|

|

Total Net Exemption |

$ |

|

|

|

|

|

|

91C (09/13)

4.TOOLS OF TRADE, IMPLEMENTS, OR PROFESSIONAL BOOKS. (NCGS

|

Market |

|

|

|

|

Net |

Description |

Value |

Lien Holder(s) |

|

|

Amt. Lien |

Value |

______________________ |

___________ |

____________________ |

|

_________ |

_______ |

|

______________________ |

___________ |

____________________ |

|

_________ |

_______ |

|

(a) Statutory allowance |

|

$ |

2,000 |

|

|

|

(b) Amount from 1(b) above to be used in this paragraph. |

|

|

|

|

||

(A part or all of 1 (b) may be used as needed.) |

$ |

|

|

|

|

|

Total Net Exemption $

5.PERSONAL PROPERTY USED FOR HOUSEHOLD OR PERSONAL PURPOSES NEEDED BY DEBTOR OR DEBTOR'S DEPENDENTS. (NCGS

|

|

Market |

|

|

|

|

|

|

|

Net |

|

Description |

|

Value |

Lien Holder(s) |

|

Amt. Lien |

Value |

|||||

Clothing & Personal |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Kitchen Appliances |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Stove |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Refrigerator |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Freezer |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Washing Machine |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Dryer |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

China |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Silver |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Jewelry |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Living Room Furniture |

___________ |

____________________ |

|

_________ |

_______ |

||||||

Den Furniture |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Bedroom Furniture |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Dining Room Furniture |

___________ |

____________________ |

|

_________ |

_______ |

||||||

Lawn Furniture |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Television |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

( ) Stereo ( ) Radio |

___________ |

____________________ |

|

_________ |

_______ |

||||||

Musical Instruments |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

( ) Piano ( ) Organ |

___________ |

____________________ |

|

_________ |

_______ |

||||||

Air Conditioner |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Paintings & Art |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Lawn Mower |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Yard Tools |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Crops |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Animals |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Other ( |

) |

___________ |

____________________ |

|

_________ |

_______ |

|||||

|

|

|

|

|

Total Net Value $ |

|

|||||

(a) Statutory allowance for debtor |

|

|

|

|

$ |

5,000 |

|

|

|

|

|

(b) Statutory allowance for debtor's dependents: |

|

|

dependents |

|

|

|

|

|

|

||

at $1,000 each (not to exceed $4,000 total for dependents) |

$ |

|

|

|

|

|

|||||

91C (09/13)

(c) Amount from 1(b) above to be used in this paragraph. |

|

|

|

|

|

|

|

|

|

||

(A part or all of 1 (b) may be used as needed.) |

$ |

|

|

|

|

|

|

||||

|

|

|

Total Net Exemption $ |

|

|

||||||

6. LIFE INSURANCE. (As provided in Article X, Section 5 of North Carolina Constitution.) |

|||||||||||

Name of Insurance Company |

|

|

|

Policy No. |

|

||||||

Name of Insured |

|

|

|

Policy Date |

|

||||||

Name of Beneficiary

7.PROFESSIONALLY PRESCRIBED HEALTH AIDS (FOR DEBTOR OR DEBTOR'S DEPENDENTS). (NCGS

Description:

__________________________________________________________________________________

8.DEBTOR'S RIGHT TO RECEIVE FOLLOWING COMPENSATION: (NCGS

A. |

$ |

|

Compensation for personal injury to debtor or to person whom debtor was dependent for support. |

B. |

$ |

|

Compensation for death of person of whom debtor was dependent for support. |

C. |

$ __________ |

Compensation from private disability policies or annuities. |

|

9.INDIVIDUAL RETIREMENT PLANS AS DEFINED IN THE INTERNAL REVENUE CODE AND ANY PLAN TREATED IN THE SAME MANNER AS AN INDIVIDUAL RETIREMENT PLAN UNDER THE INTERNAL REVENUE CODE (NCGS

DEFINED IN 11 U.S.C. § 522(b)(3)(c).

Detailed Description |

|

Value |

|

|

|

|

|

|

10.COLLEGE SAVINGS PLANS QUALIFIED UNDER SECTION 529 OF THE INTERNAL REVENUE CODE.

(NCGS

Detailed Description |

|

Value |

|

|

|

|

|

|

11.RETIREMENT BENEFITS UNDER A RETIREMENT PLAN OF OTHER STATE AND GOVERNMENTAL UNITS OF OTHER STATES, TO THE EXTEND THOSE BENEFITS ARE EXEMPT UNDER THE LAWS OF THAT STATE OR GOVERNMENTAL UNIT. (NCGS

Description:

__________________________________________________________________________________

12.ALIMONY, SUPPORT, SEPARATION MAINTENANCE AND CHILD SUPPORT. (NCGS

91C (09/13)

Description:

__________________________________________________________________________________

13.ANY OTHER REAL OR PERSONAL PROPERTY WHICH DEBTOR DESIRES TO CLAIM AS EXEMPT THAT HAS NOT PREVIOUSLY BEEN CLAIMED ABOVE. (NCGS

|

Market |

|

|

Net |

Description |

Value |

Lien Holder(s) |

Amt. Lien |

Value |

______________________ |

___________ |

____________________ |

_________ |

_______ |

______________________ |

___________ |

____________________ |

_________ |

_______ |

(a) Total Net Value of property claimed in paragraph 13. |

|

|

|

$ |

(b) Total amount available from paragraph 1(b). |

$ |

|

|

|

(c) Less amounts from paragraph 1(b) which were |

|

|

|

|

Used in the following paragraphs: |

|

|

|

|

Paragraph 3(b) |

$ |

|

|

|

Paragraph 4(b) |

$ |

|

|

|

Paragraph 5(c) |

$ |

|

|

|

Net Balance Available from paragraph 1(b) |

$ |

|||

|

Total Net Exemption |

$ |

||

14.OTHER EXEMPTIONS CLAIMED UNDER THE LAWS OF THE STATE OF NORTH CAROLINA:

Aid to the Aged, Disabled and Families with Dependent Children, NCGS

Yearly Allowance for Surviving Spouse, NCGS

North Carolina Local Government Employees Retirement Benefits, NCGS

Workers Compensation Benefits, NCGS

Unemployment Benefits, so long as not commingled and except for debts for necessities purchased while unemployed, NCGS

Group Insurance Proceeds, NCGS

Partnership Property, except on a claim against the partnership, NCGS

Other |

|

TOTAL VALUE OF PROPERTY CLAIMED AS EXEMPT |

$ |

15.EXEMPTIONS CLAIMED UNDER

Foreign Service Retirement and Disability Payments, 22 U.S.C. ' 1104 Social Security Benefits, 42 U.S.C. ' 407

Injury of Death Compensation Payments from War Risk Hazards, 42 U.S.C. ' 601 Wages of Fishermen, Seamen and Apprentices, 46 U.S.C. ' 601

Civil Service Retirement Benefits, 5 U.S.C. '' 729, 2265

Longshoremen and Harbor Workers Compensation Act Death and Disability Benefits, 33 U.S.C. ' 916

Railroad Retirement Act Annuities and Pensions 45 U.S.C. ' 228(L) Veterans Benefits, 45 U.S.C. ' 352(E)

Special Pension Paid to Winners of Congressional Medal of Honor, 38 U.S.C. ' 3101 Federal Homestead Lands, on Debts Contracted Before the Issuance of the Patent,

43 U.S.C. ' 175

Other |

|

TOTAL VALUE OF PROPERTY CLAIMED AS EXEMPT |

$ |

91C (09/13)

16.RECENT PURCHASES

The exemptions provided in NCGS

List tangible personal property purchased by the debtor less than 90 days preceding the filing of the bankruptcy petition:

|

Market |

|

|

Net |

Description |

Value |

Lien Holder(s) |

Amt. Lien |

Value |

______________________ |

___________ |

____________________ |

_________ |

_______ |

______________________ |

___________ |

____________________ |

_________ |

_______ |

DATE:

Debtor

| Fact Number | Fact Detail |

|---|---|

| 1 | The form's name is the North Carolina 91C form. |

| 2 | It pertains to the United States Bankruptcy Court for the Middle District of North Carolina. |

| 3 | Its primary purpose is to list the debtor's claim for property exemptions. |

| 4 | Exemptions are claimed pursuant to 11 U.S.C. §522(b)(3)(A), (B), and (C), North Carolina State Laws, and non-bankruptcy federal laws. |

| 5 | The form allows for the exemption of a wide variety of assets, including real estate, vehicles, personal property, and retirement accounts. |

| 6 | It outlines specific North Carolina General Statutes (NCGS) for each type of exemption claimed. | >

| 7 | Debtors may claim an exemption for the interest exceeding $125,000 in a primary residence, under certain conditions. |

| 8 | The form includes sections for exemptions under non-bankruptcy federal laws and North Carolina-specific laws. |

| 9 | Information about recent purchases made 90 days before filing for bankruptcy must be included, highlighting restrictions on certain exemptions. |

Filling out the North Carolina 91C form is a straightforward process, though it requires careful attention to detail. This form is used to claim property exemptions under various categories, ensuring certain assets are protected under the law. Both federal and state laws provide a framework for what can be exempt, so understanding which items fall under these protections will guide you through the completion of this form. Each section corresponds to a different type of exemption, from real estate and vehicles to personal household items and retirement accounts. Follow these steps closely to ensure you properly claim your exemptions.

Once completed, review the form to ensure all information is accurate and fully represents your situation regarding property exemptions. Submit the form as directed, typically to the courthouse managing your case. This form plays a crucial role in protecting your assets during legal proceedings, making accuracy and completeness paramount.

The North Carolina 91C form is a legal document used in bankruptcy proceedings. It allows individuals declaring bankruptcy in North Carolina to claim certain property as exempt from the bankruptcy estate. This means that the debtor can keep this property, up to certain limits, despite undergoing bankruptcy. The claimed exemptions are based on specific federal and state laws, including the United States Bankruptcy Code and the North Carolina General Statutes.

The exemption amount for a residence under the North Carolina 91C form is determined based on your status and the value of the property. You can exempt up to $35,000 of the net value of your residence or burial plot. If you are unmarried and 65 years of age or older, and the property was previously co-owned with a deceased spouse, you can exempt up to $60,000 of the net value. The net value is calculated by subtracting any mortgages or liens from the market value of the property. Additionally, an unused portion of the exemption, not to exceed $5,000, may be carried forward to claim an exemption in any property owned by the debtor.

Yes, under the North Carolina 91C form, you can claim exemptions for personal property used for household or personal purposes. The total exemption limit for such personal property is $5,000 for the debtor, plus an additional $1,000 for each dependent, with a maximum of $4,000 for dependents. These exemptions apply to a variety of household items and personal belongings, including clothing, kitchen appliances, furniture, and more. The specific values and exemptions are calculated by subtracting any liens from the market value of each item.

Under the "Tools of Trade" category on the North Carolina 91C form, debtors can claim exemptions for tools, implements, or professional books used in their trade or profession. The total net value of all items claimed as exempt under this category cannot exceed $2,000. This might include equipment, instruments, books, or other items that are necessary for the debtor or the debtor’s dependents' employment or business. Any unused portion of the exemption available from other categories, such as the unused portion of the homestead exemption, can be applied to increase the exemption under this category if needed.

Filling out the North Carolina 91C form, which is essential for claiming property exemptions in bankruptcy proceedings, demands precise attention to detail. However, individuals often encounter pitfalls that can significantly impact the outcome of their claims. Here are six common mistakes to avoid:

Not fully understanding the criteria for exemptions as outlined in 11 U.S.C. '522(b)(3)(A), (B), and (C), the Laws of the State of North Carolina, and non-bankruptcy federal law, leading to the incorrect application of exemption statutes.

Incorrectly calculating the market value and net value of the property. This includes overlooking outstanding liens or mortgages on properties such as homes or vehicles (real or personal property), which can result in the inaccurate reporting of assets.

Omitting necessary details about the debtor's dependents when claiming exemptions related to household or personal items needed by the debtor or the debtor's dependents (NCGS 1C-1601(a)(4)). This oversight could lead to a shortfall in exemption allowances.

Failure to properly list items under the correct categories, such as "TOOLS OF TRADE, IMPLEMENTS, OR PROFESSIONAL BOOKS" (NCGS 1C-1601(a)(5)) and "PERSONAL PROPERTY USED FOR HOUSEHOLD OR PERSONAL PURPOSES" (NCGS 1C-1601(a)(4)). Misclassification may limit the debtor's ability to maximize exemptions.

Not claiming or incorrectly calculating the "unused portion of exemption" (NCGS 1C-1601(a)(2)), which could be carried forward and applied to other properties. This mistake often occurs due to a lack of understanding of how exemptions can be strategically allocated.

Overlooking recent acquisitions and the special limitations on exemptions for recent purchases (Section 16). Failing to list tangible personal property purchased within 90 days preceding the filing may lead to disqualification of those items from exemptions.

Each mistake carries the potential to significantly impact the debtor's financial recovery through the bankruptcy process. It is critical for individuals to approach the completion of the North Carolina 91C form with thoroughness and accuracy, ensuring that all information is meticulously reviewed and correctly entered. Seeking professional advice or assistance may be beneficial to navigate these complexities effectively.

When dealing with bankruptcy filings, specifically when using the North Carolina 91C form, it's essential to gather a comprehensive set of documents and forms to ensure a thorough and accurate submission. These documents are necessary for verifying the information on the 91C form and for complying with legal requirements throughout the bankruptcy process.

Accurate and complete documentation is crucial for a successful bankruptcy filing. The North Carolina 91C form, alongside these documents, provides the court with a full picture of the debtor's financial situation, ensuring that all parties understand the scope of the exemptions claimed. Each piece of documentation plays a vital role in the process, helping to streamline the proceeding and ensuring that the debtor’s rights are protected.

The North Carolina 91C form is analogous to the Schedule C form used in federal bankruptcy cases across the United States. Both documents serve the critical function of allowing a debtor to list and claim exemptions for their property under applicable laws. Schedule C, like the North Carolina 91C form, enables individuals filing for bankruptcy to protect certain assets from being liquidated by trustees to pay creditors. The similarities lie in the structure of listing properties, specifying legal statutes for exemptions, and noting the claimed value of each exempt asset, providing a safeguard for debtors' essential items or properties.

Another similar document is the Homestead Declaration form found in various states, which is designed to protect a portion of a debtor’s home equity from creditors. While the North Carolina 91C form encompasses a broad array of property types, including homestead exemptions, the Homestead Declaration specifically focuses on real estate used as a primary residence. Both documents embody the principle of permitting debtors to retain essential living necessities notwithstanding financial distress, albeit through slightly different legal mechanisms and with a difference in scope.

The Motor Vehicle Exemption form, used in several jurisdictions, resembles the section of the North Carolina 91C form that allows for the exemption of one motor vehicle per debtor. Both forms necessitate the debtor to detail the vehicle’s make, model, value, and encumbrances to calculate the net exempt value, typically capped at a specific amount. This comparison illustrates how state-specific forms, like North Carolina’s, integrate various exemption categories into one comprehensive document for bankruptcy protection purposes.

Tools of the Trade exemption forms are closely related to Section 4 of the North Carolina 91C, which pertains to professional tools and books. Both types of documents enable individuals to exempt equipment and materials crucial for their livelihood, thereby ensuring that bankruptcy does not deprive them of their ability to earn income. They require detailed listings of such items along with their values and any liens against them, reflecting a shared goal of balancing creditor rights with debtor needs for economic rehabilitation.

The Wild Card Exemption form, available in some jurisdictions, offers flexibility similar to the unused exemption portion of the North Carolina 91C form. It allows debtors to exempt any property up to a certain value, providing a safety net for assets that do not fit into other specific exemption categories. This approach underscores a system that accommodates the diverse assets individuals may possess, prioritizing the preservation of a debtor's financial foundation post-bankruptcy.

Personal Property Exemption forms are akin to the personal property section within the North Carolina 91C form, which covers household goods, furnishings, and personal effects. These documents are fundamental in protecting items that ensure a basic standard of living, specifying allowable items and exemption limits. The comparability underlines a shared legal recognition across jurisdictions of the intrinsic value of personal belongings in maintaining a minimal quality of life.

Life Insurance Exemption forms parallel the segment in the North Carolina 91C form that addresses life insurance policies. Both documents ensure that life insurance proceeds, which are meant to provide financial security for the debtor's dependents, are shielded from creditors. This aspect of exemption law reflects a common understanding of the importance of preserving future financial stability for a debtor's family.

The Wages Exemption form, present in some states, bears resemblance to the earnings protection provided under the North Carolina 91C form, albeit indirectly through other exemptions. While the North Carolina form doesn’t have a distinct wage exemption category, it contributes to the same objective: preventing the total stripping away of a debtor's means of support. This underscores a fundamental bankruptcy protection principle — allowing individuals to retain enough resources to meet essential needs despite debts.

Finally, the retirement accounts exemption forms, similar to Section 9 of the North olina 91C form, focus on safeguarding retirement benefits from creditors. Both recognize the critical importance of securing a debtor's financial independence in retirement, exempting various types of retirement accounts and pensions. This similarity across documents reflects a widespread legal acknowledgment of the need to protect long-term financial planning from the immediate demands of creditors.

When you're filling out the North Carolina 91C form, it’s important to navigate the process with accuracy and caution. This form is designed to help you claim property exemptions under various laws, including federal statutes and the laws of North Carolina. To ensure you're doing it correctly, here's a list of dos and don’ts:

Do:

Read the instructions carefully before you start filling out the form. Understanding each section fully can help prevent mistakes.

Ensure that you accurately list the description and value of the property you claim as exempt. It’s important to be honest and precise to avoid issues down the line.

Consult with a legal advisor if you're unsure about any part of the form. Legal nuances can greatly impact your exemptions.

Check if you are eligible for exemptions that require specific criteria, such as being 65 years or older for certain property exemptions.

Use the additional space or attach extra sheets if the provided space is insufficient to list all your exempt properties.

Sign and date the form at the end. Your signature is required to process the document.

Keep a copy of the filled-out form for your records. This can be helpful for future reference or if any disputes arise.

Don't:

Don’t rush through filling out the form. Take your time to ensure all information is correct.

Avoid guessing the value of your assets. Use recent statements or get appraisals if necessary to provide accurate figures.

Don’t overlook the exemptions for which you may be eligible under non-bankruptcy federal law. These can offer additional protections.

Avoid listing ineligible property as exempt. This could lead to complications or challenges during the bankruptcy process.

Don’t forget to claim exemptions for professionally prescribed health aids, if applicable. These are crucial for your well-being and are fully exempt.

Avoid leaving any required field blank. If a section doesn’t apply to you, mark it as "N/A" or "Not Applicable."

Don’t submit the form without reviewing it for accuracy and completeness. A final check can prevent errors.

By following these guidelines, you can ensure that you accurately complete the North Carolina 91C form, helping to protect your assets to the fullest extent permitted under the law.

When it comes to navigating the complexities of bankruptcy exemptions in North Carolina, the 91C form is a critical tool for debtors. However, there are several misconceptions about this form and its use. Understanding these misconceptions is key to accurately claiming exemptions and protecting one's property during bankruptcy proceedings.

Only real estate can be exempted: Many people mistakenly believe the 91C form is exclusively for real estate exemptions. In reality, it encompasses a wide range of property types, including vehicles, household goods, tools of the trade, and more.

Exemptions are automatic: Another misconception is that exemptions on the 91C form are automatic once filed. Debtors must accurately list and claim exemptions; failing to do so may result in losing those exemptions.

Unlimited exemptions for personal property: It's wrongly assumed that there's no limit to the value of personal property that can be exempted. However, the law sets specific caps on various categories, such as household goods and tools of trade.

All debts are covered: Some believe that claiming exemptions on the 91C form means protection against all types of debts. While exemptions can protect against many debts, they do not shield against secured debts where the property is collateral.

91C form is the only step in the exemption process: Filing the 91C form is an important step, but it's not the only one. Debtors also need to navigate additional paperwork and possibly court hearings to fully protect their property.

One size fits all: There's a misconception that the exemption amounts and categories are the same for everyone. Factors such as marital status, age, and whether dependents exist can affect exemption amounts and eligibility.

The $125,000 cap applies to all property: The confusion that the $125,000 exemption cap applies generally, when in fact, it specifically relates to property used as a residence.

No need for detailed descriptions: A common mistake is providing vague descriptions of property. Detailed descriptions and values are crucial for accurately claiming exemptions and preventing challenges.

Correcting these misconceptions about the North Carolina 91C form is fundamental for debtors aiming to make informed decisions about their bankruptcy exemptions. This clarity can significantly impact the outcome of bankruptcy proceedings, safeguarding one’s financial future.

Understanding and completing the North Carolina 91C form is crucial for individuals facing bankruptcy. This form allows debtors to claim certain properties as exempt, meaning they are shielded from being used to pay off creditors. Here are four key takeaways to consider:

Navigating the complexities of the 91C form is a vital part of the bankruptcy process in North Carolina. Properly claiming exemptions can offer a lifeline to debtors, allowing them to retain essential assets as they work through financial challenges. As such, careful attention to detail and a thorough understanding of applicable laws are indispensable.

Nc Workers Comp - By signifying the employer's admission, it sets the stage for subsequent required actions, such as compensation payments and medical treatment coverage for the injured or ill employee.

D422 - The form serves as a reminder of the critical deadlines for estimated tax payments, helping individuals to plan their finances accordingly.