Fillable D 422 North Carolina Template

Fillable D 422 North Carolina Template

The North Carolina Department of Revenue issues Form D-422 for individuals to calculate and assess potential penalties on underpaid estimated taxes. Designed to guide taxpayers through this process, the form is critical for those navigating their financial responsibilities to avoid unintended fines. The necessity to use Form D-422 emerges from the complexity of tax regulations and the common occurrence of underpayment of estimated taxes. By providing a structured way to determine the required annual payment and any applicable penalties, the form aids taxpayers in rectifying discrepancies before they lead to larger issues. Taxpayers can choose between two methodologies—short and regular—based on their payment history and specific circumstances, including exceptions like farmers and fishermen who have their own set of rules. Moreover, instructions included with the form, such as calculation adjustments for income variance and handling of withheld taxes, make it easier to comply with state tax laws accurately. Especially for those who did not owe a penalty in the previous year or their estimated tax payments varied throughout the year, understanding the nuances of Form D-422 is crucial. By completing either Part II or Part III, taxpayers can determine the exact penalty owed, if any, ensuring they fulfill their obligations while potentially minimizing unnecessary costs.

(Rev. |

|

1998 |

Form |

NORTH CAROLINA DEPARTMENT OF REVENUE |

|

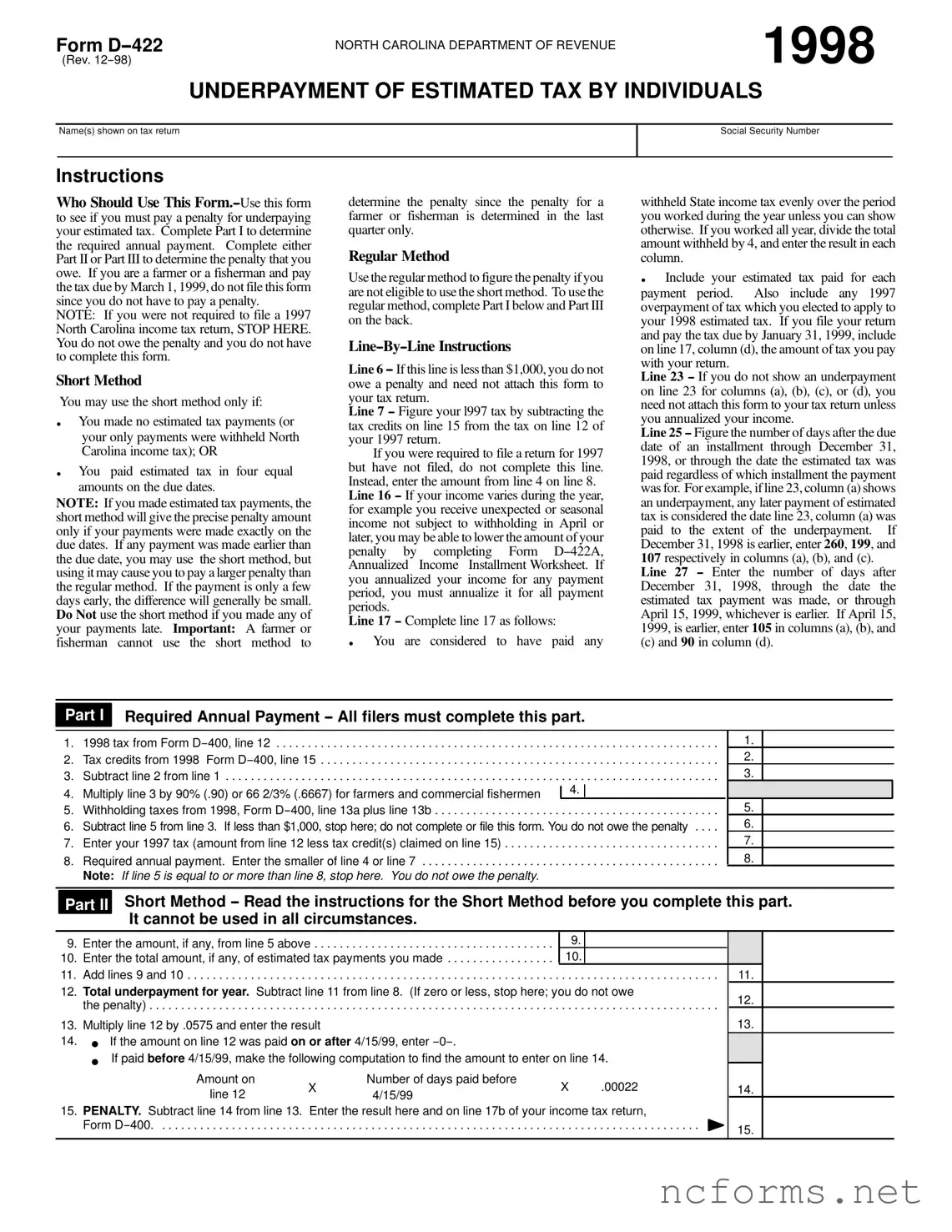

UNDERPAYMENT OF ESTIMATED TAX BY INDIVIDUALS

Name(s) shown on tax return

Social Security Number

Instructions

Who Should Use This

NOTE: If you were not required to file a 1997 North Carolina income tax return, STOP HERE. You do not owe the penalty and you do not have to complete this form.

Short Method

You may use the short method only if:

. You made no estimated tax payments (or your only payments were withheld North Carolina income tax); OR

. You paid estimated tax in four equal amounts on the due dates.

NOTE: If you made estimated tax payments, the short method will give the precise penalty amount only if your payments were made exactly on the due dates. If any payment was made earlier than the due date, you may use the short method, but using it may cause you to pay a larger penalty than the regular method. If the payment is only a few days early, the difference will generally be small. Do Not use the short method if you made any of your payments late. Important: A farmer or fisherman cannot use the short method to

determine the penalty since the penalty for a farmer or fisherman is determined in the last quarter only.

Regular Method

Use the regular method to figure the penalty if you are not eligible to use the short method. To use the regular method, complete Part I below and Part III on the back.

Line 6

Line 7

If you were required to file a return for 1997 but have not filed, do not complete this line. Instead, enter the amount from line 4 on line 8.

Line 16

Line 17

. You are considered to have paid any

withheld State income tax evenly over the period you worked during the year unless you can show otherwise. If you worked all year, divide the total amount withheld by 4, and enter the result in each column.

. Include your estimated tax paid for each

payment period. Also include any 1997 overpayment of tax which you elected to apply to your 1998 estimated tax. If you file your return and pay the tax due by January 31, 1999, include on line 17, column (d), the amount of tax you pay with your return.

Line 23

Line 25

Line 27

(c) and 90 in column (d).

Part I

Required Annual Payment

1. |

1998 tax from Form |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

2. |

Tax credits from 1998 Form |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

3. |

Subtract line 2 from line 1 |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

4. |

Multiply line 3 by 90% (.90) or 66 2/3% (.6667) for farmers and commercial fishermen |

|

4. |

|

|

|

|||

5. |

Withholding taxes from 1998, Form |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

6. |

Subtract line 5 from line 3. If less than $1,000, stop here; do not complete or file this form. You do not owe the penalty . . . . |

|||

7. |

Enter your 1997 tax (amount from line 12 less tax credit(s) claimed on line 15) |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

8. |

Required annual payment. Enter the smaller of line 4 or line 7 |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

|

Note: If line 5 is equal to or more than line 8, stop here. You do not owe the penalty. |

|

|

|

1.

2.

3.

5.

6.

7.

8.

Part II

Short Method

9. |

Enter the amount, if any, from line 5 above |

9. |

|

|

|||

10. |

Enter the total amount, if any, of estimated tax payments you made |

10. |

|

|

|||

11. |

Add lines 9 and 10 |

11. |

|||||

12. |

Total underpayment for year. Subtract line 11 from line 8. (If zero or less, stop here; you do not owe |

12. |

|||||

|

the penalty) |

||||||

|

|

||||||

13. |

Multiply line 12 by .0575 and enter the result |

|

|

|

13. |

||

14. |

. |

If the amount on line 12 was paid on or after 4/15/99, enter |

|

|

|

||

|

. |

If paid before 4/15/99, make the following computation to find the amount to enter on line 14. |

|

||||

|

Amount on |

|

Number of days paid before |

|

|

|

|

|

|

X |

X |

.00022 |

14. |

||

|

|

line 12 |

4/15/99 |

||||

|

|

|

|

|

|

||

15. |

PENALTY. Subtract line 14 from line 13. |

Enter the result here and on line 17b of your income tax return, |

|

||||

|

Form |

15. |

|||||

|

|

|

|

|

|

|

|

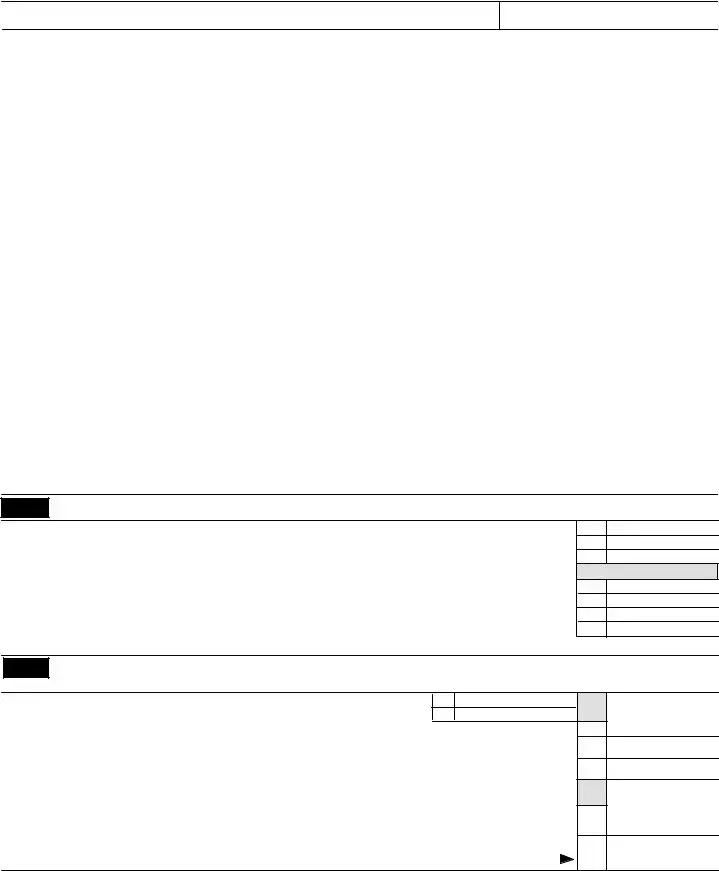

Form

Page 2

|

Part III |

Regular Method |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Section A |

|

|

Payment Due Dates |

|

||

|

|

(a) |

(b) |

(c) |

(d) |

||

|

|

|

|

4/15/98 |

6/15/98 |

9/15/98 |

1/15/99 |

16.Divide line 8 by 4 and enter the result in each column. Exception: If you use the annualized income

|

ment method, complete Form |

|

16. |

|

|

||||

17. |

Income Installment Worksheet) and check this box. |

|

|

|

|

|

|||

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

Estimated tax paid and tax withheld. For column (a) only, |

|

|

|

|

|

||||

|

|

|

|

|

|

||||

|

enter the amount from line 17 on line 21. (If line 17 is |

|

|

|

|

|

|||

|

equal to or more than line 16 for each payment period, |

17. |

|

|

|||||

|

. . . .stop here; you do not owe the penalty.) |

|

|

||||||

|

|

|

|||||||

|

Complete lines 18 through 24 of one column before |

|

|

|

|

|

|||

|

going to the next column. |

|

|

|

|

|

|||

18. |

Enter amount, if any, from line 24 of previous colum . . . . |

18. |

|

|

|||||

|

|

19. |

|

|

|||||

19. |

Add lines 17 and 18 |

|

|

||||||

20. |

Add amounts on lines 22 and 23 of the previous column |

|

|

and enter the result |

20. |

21.Subtract line 20 from line 19 and enter the result. If zero

or less, enter zero. (For column (a) only, enter the |

|

amount from line 17) |

21. |

22.Remaining underpayment from previous period. If the

amount on line 21 is |

||

and enter the result. Otherwise, enter |

. . . . 22. |

|

23. Underpayment. If line 16 is larger than or equal |

to |

|

line 21, subtract line 21 from line 16 and enter the |

||

result. Enter 0 on line 18 of the next column and go to |

||

line 19. Otherwise, go to line 24 |

. . . . 23. |

|

24.Overpayment. If line 21 is larger than line 16, subtract

|

|

line 16 from line 21 and enter the result. Then go to |

|

|

|

|

|

|

|||||

|

|

line 18 of next column. . |

. . . . . . . . . . . . . . . . . . . . |

. . . . |

. . . . 24. |

|

|

|

|

||||

|

Section B Figure the Penalty (Complete lines 25 through 28 of one column before going to the next |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

April 15, 1998 December 31, 1998 |

|

|

|

|

|

|

|

||||

|

|

|

|

|

4/15/98 |

6/15/98 |

9/15/98 |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||

|

25. Number of days after the date shown above line 25 through |

|

Days: |

Days: |

Days: |

|

|||||||

|

|

the date the amount on line 23 was paid or |

12/31/98, |

|

|

|

|

|

|||||

|

|

whichever is earlier. |

. . . . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . |

25. |

|

|

|

|

|||

|

26. |

Underpayment |

X |

|

Number of days |

X |

.09 |

|

|

|

|

|

|

|

|

on line 23 |

|

on line 25 |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

(see instructions) |

|

365 |

|

|

|

26. |

$ |

$ |

$ |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

January 1, 1999 |

April 15, 1999 |

|

|

|

|

|

|

|

|||

|

|

|

|

|

12/31/98 |

12/31/98 |

12/31/98 |

1/15/99 |

|||||

|

|

|

|

|

|

|

|

|

|

||||

|

27. Number of days after the date shown above line 27 through |

|

Days: |

Days: |

Days: |

Days: |

|||||||

|

|

the date the amount on line 23 was paid or |

4/15/99, |

|

|

|

|

|

|||||

|

|

whichever is earlier. |

. . . . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . |

27. |

|

|

|

|

|||

|

28. |

Underpayment |

X |

|

Number of days |

X |

.08 |

|

|

|

|

|

|

|

|

on line 23 |

|

on line 27 |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

(see instructions) |

|

365 |

|

|

|

28. |

$ |

$ |

$ |

$ |

|

|

|

|

|

|

|

|

|

|

|||||

29.Penalty (add amounts on line 26 and 28). Enter here and on line 17b of your individual income tax return,

Form

29.

| Fact | Detail |

|---|---|

| Form Title | Form D-422 |

| Revision Date | December 1998 |

| Purpose | To determine if an individual must pay a penalty for underpaying their estimated tax in North Carolina |

| Applicability | Individuals who did not pay enough estimated tax throughout the year |

| Short Method Eligibility | Individuals who made no estimated tax payments, or whose only payments were withheld state income tax, and those who paid in four equal amounts on the due dates |

| Regular Method Usage | Recommended if not eligible for the Short Method or accurate calculation is needed beyond the Short Method's scope |

| Special Consideration for Farmers and Fishermen | No penalty if tax due is paid by March 1, 1999; cannot use the Short Method for penalty calculation |

| Governing Law | North Carolina Department of Revenue Guidelines |

Fulfilling tax obligations accurately and on time is paramount to avoiding penalties levied by tax authorities. In North Carolina, residents who underpay their estimated tax are potentially subject to a penalty. To ascertain whether you're on the hook for such a penalty, and if so, how much you owe, you'd fill out Form D-422. This form, issued by the North Carolina Department of Revenue, guides individuals through calculating underpayment and assessing penalties. Suitable understanding and meticulous attention to detail are needed as you navigate through its sections, ensuring precision in your submission.

Accuracy, timeliness, and an understanding of your tax situation are all critical when handling potential underpayment penalties. By carefully following the outlined steps and meticulously entering the correct information on Form D-422, you can ensure that your obligations are met in accordance with North Carolina tax regulations.

Individuals who might have underpaid their estimated tax need to use the D-422 form. Specifically, if you didn't file a North Carolina income tax return for 1997, or if you're a farmer or fisherman who paid taxes by March 1, 1999, this form isn't necessary. Essentially, if there's a chance you've paid less estimated tax than required, this form helps to determine if you owe a penalty.

Yes, but only under certain conditions. The short method is suitable if you either made no estimated tax payments or made payments in four equal amounts on the scheduled due dates. It's an easier way to calculate the penalty, but might result in paying a slightly higher penalty than using the regular method, especially if payments were made earlier than the due dates.

Farmers and fishermen cannot use the short method since their penalty is calculated only in the last quarter. Additionally, if any of your estimated payments were made late, this method is also not suitable for you.

If your income was not consistent, filling out the D-422A, Annualized Income Installment Worksheet, might help reduce your penalty amount. This approach requires you to annualize your income for each payment period, potentially lowering your penalty if you had fluctuations in your earnings.

If, upon calculation, your underpayment amount is less than $1,000, you're in luck, as you do not owe a penalty. This waiver ensures minor underpayments don't get unnecessarily penalized.

Generally, you need to attach this form to your tax return if it shows an underpayment. However, if your form does not show any underpayment for the payments made, and you didn't annualize your income, then you do not need to attach this form. It's designed to determine penalty, so no penalty means no need for attachment, with the exception of cases involving income annualization.

Not determining eligibility accurately: Individuals often skip verifying whether they are required to pay a penalty for underpaying estimated taxes, leading to unnecessary form fill-outs or missed penalties.

Choosing the wrong calculation method: The form allows for both a short and a regular method. Making the choice without fully understanding each option's criteria can lead to inaccuracies in calculated penalties.

Incorrect annual payment calculation: Input errors or misunderstandings in calculating the required annual payment under Part I can significantly affect the rest of the form.

Misinterpreting the income variability provision: When income varies, especially for individuals with unexpected or seasonal income, incorrectly applying the rules of Form D-422A can result in an incorrect penalty amount.

Omitting withheld state income tax adjustments: Failing to consider the evenly spread assumption of withheld taxes over the work period can lead to miscalculations in credits toward the estimated tax.

Errors in estimated tax payments entry: Incorrectly reporting the amounts or timing of estimated tax payments, including any overpayment from the previous year intended for the current year’s estimated tax, alters the accuracy of computed penalties.

Overlooking changes in installment payments due to early or late payments: Not adjusting the payment periods correctly for early or late payments of estimated taxes can lead to incorrect penalty calculations, especially when using the short method.

Miscalculation of days for penalty calculation: Both underestimating and overestimating the number of days overdue for an installment can drastically change the penalty amount, whether calculating penalties up to December 31 or until the tax was paid.

Failure to apply for penalty waivers when eligible: Certain situations, like being a farmer or fisherman with specific deadlines, can exempt an individual from penalties. Not understanding these exceptions can lead to unnecessary penalty payments.

Incorrect final penalty calculation: Both under and over-calculation of the final penalty, due to inaccuracies in earlier sections or failure to apply the correct interest rates for penalties, can result in incorrect amounts being reported.

When dealing with taxes, especially concerning the underpayment of estimated taxes by individuals, the process often requires more than just filling out Form D-422 in North Carolina. Various other forms and documents play a crucial role in ensuring compliance and accuracy in tax filings. Understanding these documents can help individuals navigate the complexities of tax regulations more effectively.

Each of these documents serves a unique purpose in the broader context of tax preparation and filing. By familiarizing themselves with these forms, taxpayers in North Carolina can ensure they meet their tax obligations accurately and efficiently, potentially avoiding penalties and maximizing their eligible deductions and credits.

The Form 1040-ES, "Estimated Tax for Individuals," closely relates to the Form D-422. Both documents are designed for individuals to calculate and pay their estimated taxes throughout the year. They share the goal of avoiding underpayment penalties by assisting taxpayers in estimating their income tax liability and making quarterly payments. However, Form 1040-ES applies to federal income tax, while Form D-422 is specific to North Carolina state income tax.

The Form 2210, "Underpayment of Estimated Tax by Individuals, Estates, and Trusts," serves a similar purpose to Form D-422, albeit on a federal level. It helps taxpayers determine whether they owe a penalty for underpaying estimated taxes and calculate the amount of such a penalty. Like the D-422, Form 2210 includes a provision for annualized income, which allows for a more accurate penalty calculation for those who do not receive their income evenly throughout the year.

Form IT-2105, "Estimated Tax Payment Voucher for Individuals," used by the New York State Department of Taxation and Finance, resembles the D-422. This document facilitates the payment of estimated tax on income that is not subject to withholding. Both forms cater to individuals who need to make quarterly estimated tax payments to avoid underpayment penalties.

The Form 540-ES, "Estimated Tax for Individuals," is the California equivalent of North Carolina's D-422 form. It is designed for taxpayers in California to submit their estimated tax payments. Like the D-422, this form helps prevent underpayment penalties by calculating the proper quarterly payments based on the taxpayer's estimated income for the year.

Form IL-1040-ES, "Estimated Income Tax Payments for Individuals," provided by the Illinois Department of Revenue, parallels the functionalities of North Carolina's D-422. It assists Illinois taxpayers in determining the estimated tax owed throughout the tax year to avoid penalties similar to those calculated on Form D-422 for North Carolina residents.

The Form PA-40ES, "Individual Estimated Personal Income Tax," is utilized by Pennsylvania individuals who anticipate owing tax on income not covered by withholdings. Similar to the D-422, the PA-40ES form is tailored for residents to estimate their tax liability and make quarterly payments, effectively managing their tax obligations to prevent underpayment penalties.

Form NJ-1040-ES, "Estimated Tax Voucher," is intended for New Jersey residents to estimate and pay their tax on income not subject to withholding. Its purpose aligns with North Carolina's D-422 form in facilitating the process of calculating and paying estimated taxes on a quarterly basis, thereby avoiding penalties for underpayment.

Form VA-4P, "Withholding Certificate for Pension or Annuity Payments," although more specific in its application, shares the concept of adjusting tax payments according to estimated tax liability with the D-422. Both forms aim at ensuring individuals meet their tax liabilities in a timely and accurate manner, though the VA-4P focuses on pension or annuity payments.

The Form 760ES, "Virginia Estimated Income Tax Payment Vouchers for Individuals," is another state-specific document similar to the D-422, dedicated to Virginia residents. This form guides taxpayers through calculating and making their estimated tax payments, a process necessary for income not covered by withholding, to mitigate penalties for underpayment.

Lastly, Form M1W, "Minnesota Income Tax Withheld," although primarily a withholding tax form, indirectly relates to the process of managing tax payments through withholdings. Like the D-422, it plays a role in ensuring individuals' compliance with tax obligations, albeit through the lens of documenting withheld taxes rather than estimating future payments.

Filling out the D-422 North Carolina form, designed to determine if you owe a penalty for underpaying estimated taxes, calls for meticulous attention to detail and an understanding of tax regulations. To assist you in accurately completing this form, here are some practical dos and don'ts:

Do:By adhering to these guidelines, you can navigate the completion of the D-422 form with confidence—and possibly avoid or minimize any penalties for underpayment of estimated taxes.

Many people have misconceptions about the North Carolina Form D-422, which is used for calculating the penalty for underpayment of estimated tax. Understanding these misconceptions is crucial for accurately completing the form and avoiding unnecessary penalties. Here are six common misunderstands and clarifications for each.

Correcting these misconceptions ensures that individuals can navigate their tax responsibilities with greater accuracy and confidence, potentially avoiding unnecessary penalties by understanding the specifics of when and how to use Form D-414 correctly.

Filling out and using the D 422 North Carolina form, a critical document for those navigating the realm of estimated tax payments, can indeed seem daunting at first glance. However, understanding its primary functions and key takeaways can simplify the process, ensuring individuals meet their tax obligations accurately and avoid unnecessary penalties. Here are four significant takeaways to guide taxpayers through this process effectively:

Overall, the D 422 form serves as a crucial instrument for North Carolina residents managing their estimated tax payments. By clarifying when a penalty is due and offering methodologies to calculate said penalty, it supports taxpayers in fulfilling their obligations while potentially minimizing unnecessary payouts. Remember, understanding the key elements and instructions of the D 422 form can significantly ease the process of estimating tax payments and addressing underpayment penalties.

Reporting Forms - The form’s revision date signals to employers the most current version and requirements for reporting new hires.

North Carolina Driving License - Facilitates conditional driving ability for individuals in North Carolina with convictions like impaired driving, focusing on rehabilitation.